The Thrift Savings Plan (TSP)

A Powerful Federal Retirement Tool

What Hidden Trade-Offs You Should Understand

The Thrift Savings Plan is the retirement account designed specifically for federal employees and members of the uniformed services. It functions much like a 401(k), letting you save through payroll deductions while enjoying tax advantages and low fees. For many, it’s the cornerstone of retirement planning, but understanding its limitations is just as important as knowing its benefits.

How the TSP Works

You can contribute to the TSP in two ways:

Traditional TSP – Contributions reduce your taxable income today. Your money grows tax-deferred, and withdrawals in retirement are taxed as ordinary income.

Roth TSP – Contributions are made with after-tax dollars, but qualified withdrawals in retirement, including growth, are tax-free.

Either way, your TSP funds grow over time, leveraging the power of compound interest.

TSP Investment Options at a Glance

The TSP keeps investing simple, with just a few core choices:

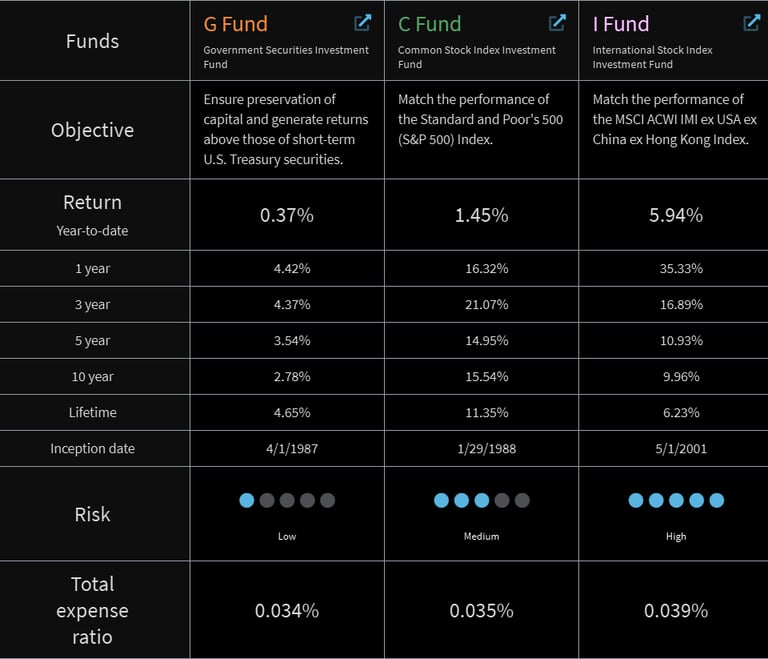

G Fund – Government securities; lowest risk, stable growth.

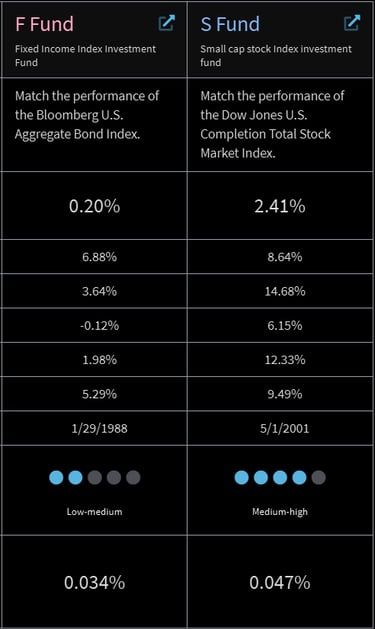

F Fund – Bonds; moderate risk and steady growth.

C Fund – Large-cap U.S. stocks (S&P 500 index).

S Fund – Small and mid-cap U.S. stocks.

I Fund – International stocks.

L Funds – Target-date funds that automatically adjust allocations as you near retirement.

While the TSP’s simplicity is convenient, its limited options can restrict potential growth or customization for your unique retirement strategy.

Contributions, Matching & Limits

Employee Contributions: Up to IRS annual limits (same as 401(k)/IRA).

Catch-Up Contributions: Available for employees age 50 and older.

Employer Match (FERS employees): 1% automatic + up to 4% additional on contributions.

Military Employees (BRS): Matching contributions available after 2 years of service.

Automatic payroll contributions make saving effortless—but knowing how much to contribute and which fund mix to choose is key to maximizing your TSP

Taxes & Withdrawals: What You Need to Know

Traditional TSP: Tax-deferred growth, taxed as ordinary income on withdrawal.

Roth TSP: After-tax contributions, tax-free withdrawals if rules are met.

Required Minimum Distributions (RMDs): Start at age 73 for Traditional TSP.

Early Withdrawals: Restricted before age 59½; penalties may apply.

Tax rates today may be historically low, but they can rise by the time you retire. Relying solely on pre-tax contributions could leave you paying more than expected in the future.

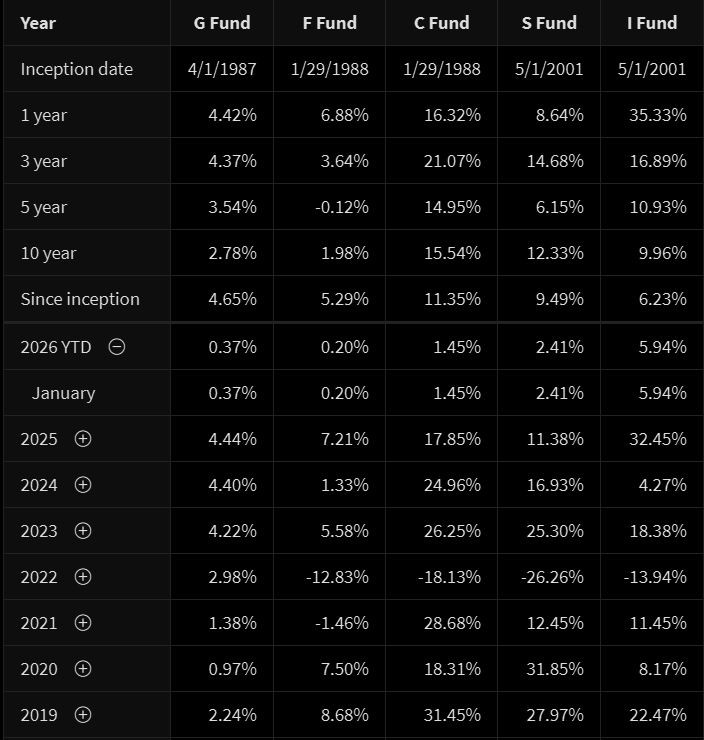

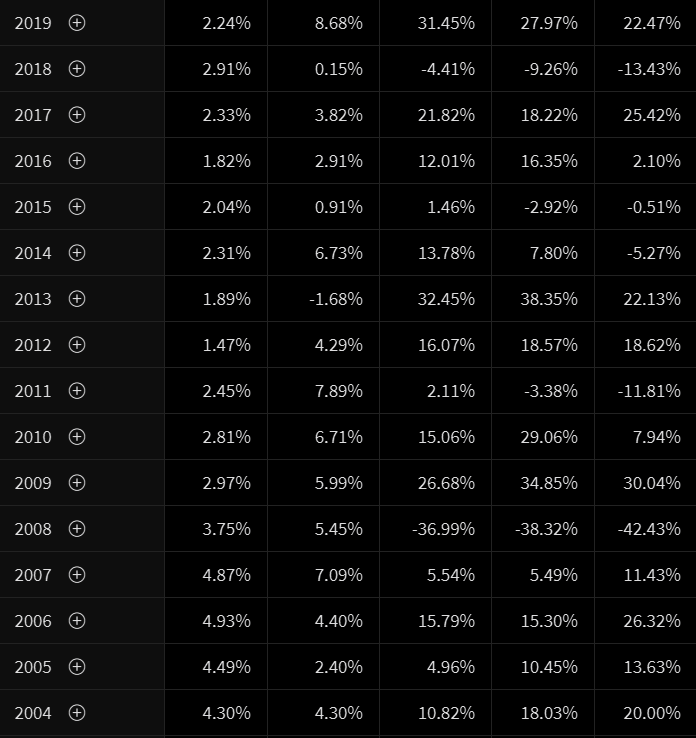

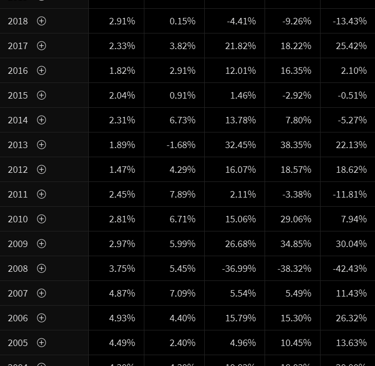

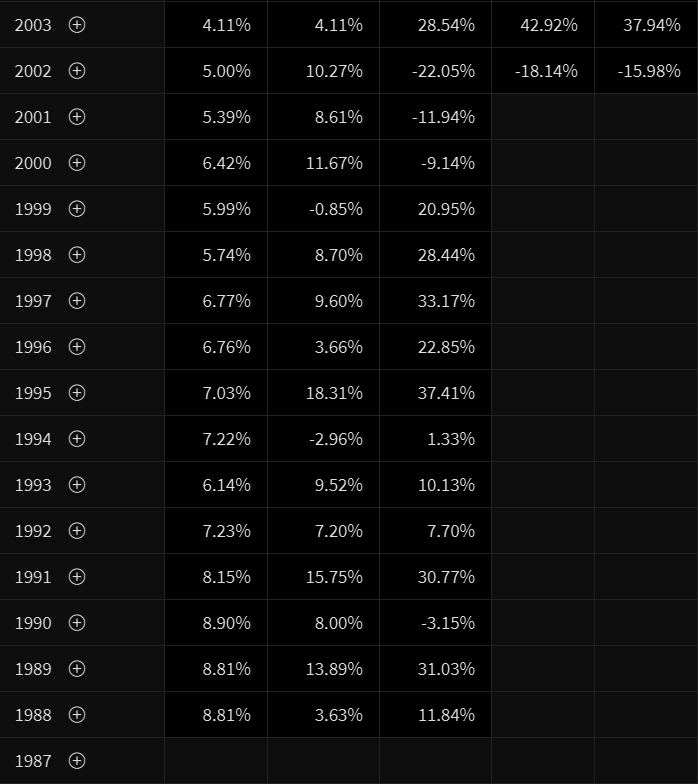

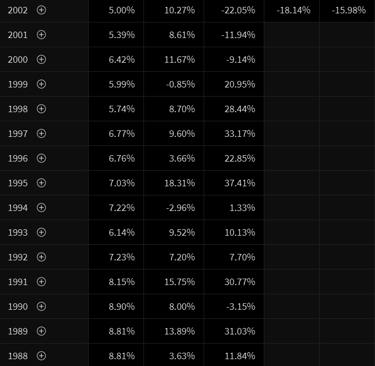

Above are the posted returns for each individual fund over the years pulled directly from https://www.tsp.gov/fund-performance/

Pros of the TSP

Extremely low fees compared to most retirement accounts

Employer matching contributions help accelerate growth

Simple, structured, and automatic saving

Roth option provides future tax-free withdrawals

Easy to manage, especially for federal employees juggling other responsibilities

Cons & Limitations

Limited investment options; less flexibility than an IRA or brokerage account

Withdrawals taxed as ordinary income (Traditional TSP)

Required Minimum Distributions apply to Traditional TSP

Loans and early withdrawals are restricted

May not fully address future tax concerns or legacy planning

While the TSP is a solid foundation, many federal employees supplement it with other strategies to create more balanced, tax-efficient retirement income.

Common Misconceptions

“Taxes will be lower when I retire.” Not guaranteed—federal retirees may face combined pension, Social Security, and TSP withdrawals that push them into higher brackets.

“The G Fund is completely safe.” It’s low-risk, but growth is modest.

“Roth TSP means no taxes ever.” True only if contributions and withdrawals follow all IRS rules.

When You Might Need More Than the TSP

While the TSP is a strong foundation, it doesn’t provide full flexibility or guaranteed tax-free income. Many federal employees explore supplemental strategies to:

Diversify tax exposure in retirement

Create guaranteed income streams

Maximize flexibility and control for wealth transfer

Your TSP is powerful... but pairing it with smart strategies outside the plan can help you retire with confidence, security, and tax efficiency.

Follow us on Social

Get updates on new ventures through Social Media

Contact

info@leveraged-financial.com

(518) 480-8848

© 2026. All rights reserved.